One Big Beautiful Bill Act 2025: Complete Guide for Colorado Springs Small Business Owners

On July 4, 2025, President Trump signed the One Big Beautiful Bill Act (OBBBA) into law, ushering in the most significant tax changes since the 2017 Tax Cuts and Jobs Act. This sweeping 870-page legislation permanently extends many business-friendly tax provisions while introducing new deductions that could save Colorado Springs small businesses thousands of dollars annually. As your trusted CPAs serving El Paso County for nearly 40 years, we've analyzed every provision to help you understand exactly how these changes impact your bottom line—and what actions you need to take now to maximize your tax savings.

Critical Action Required

Legislative History: How We Got Here

The One Big Beautiful Bill Act represents the culmination of months of negotiations in the 119th United States Congress. After passing the House of Representatives 218-214 on July 3, 2025, the bill narrowly cleared the Senate 51-50 on July 1, with Vice President JD Vance casting the tie-breaking vote. President Trump signed the legislation on Independence Day 2025, making it Public Law 119-21.

This reconciliation bill addresses the impending expiration of TCJA provisions scheduled for December 31, 2025, while implementing President Trump's campaign promises including "no tax on tips" and "no tax on overtime." The legislation includes both permanent changes and temporary provisions set to expire in 2028 or 2030, creating a complex landscape that Colorado Springs business owners must navigate carefully.

Planning Opportunity

Major Business Tax Provisions: What Changed

100% Bonus Depreciation (Permanent)

The OBBBA permanently restores 100% bonus depreciation for qualified property acquired on or after January 20, 2025. This reverses the scheduled phase-down that would have reduced bonus depreciation to 40% in 2025, 20% in 2026, and 0% in 2027.

What This Means for Colorado Springs Businesses:

- Immediate full deduction for qualifying equipment, vehicles, and machinery

- Applies to both new and used property (if new to your business)

- No dollar limit on total bonus depreciation claimed

- Retroactive to January 20, 2025 for current-year purchases

Example: Equipment Purchase

A Colorado Springs construction company purchases $500,000 in equipment on March 1, 2025. Under old rules, they'd deduct $200,000 (40% in 2025). With the OBBBA, they can deduct the full $500,000 immediately, potentially saving $150,000+ in federal taxes.

Important Considerations:

- Property must be acquired and placed in service during the same tax year

- Original use must begin with the taxpayer (except for used property meeting specific requirements)

- Special rules apply for certain aircraft and luxury vehicles

- Businesses should evaluate bonus depreciation versus Section 179 for optimal tax planning

Enhanced Section 179 Expensing

Section 179 expensing limits have been significantly increased under the OBBBA, providing immediate tax relief for equipment purchases:

| Tax Year | Maximum Deduction | Phase-Out Threshold | Total Equipment Limit |

|---|---|---|---|

| 2024 | $1,220,000 | $3,050,000 | $4,270,000 |

| 2025-2026 | $2,500,000 | $4,000,000 | $6,500,000 |

| 2027+ | Indexed for inflation | Indexed for inflation | Indexed for inflation |

Key Differences Between Section 179 and Bonus Depreciation:

Section 179 vs. Bonus Depreciation Decision Matrix

Permanent 20% QBI Deduction (Section 199A)

The OBBBA makes permanent the Qualified Business Income (QBI) deduction, which was originally scheduled to expire after 2025. This 20% deduction for pass-through business income now includes important enhancements:

Major Changes to QBI Deduction:

- New Minimum Deduction: Taxpayers with at least $1,000 of QBI from an active trade or business receive a minimum $400 deduction (indexed for inflation after 2026)

- Expanded Phase-In Ranges: Income limits increased from $100,000 to $150,000 for married filing jointly

- Permanent Status: No more year-to-year uncertainty about expiration

2026 QBI Phase-Out Thresholds:

| Filing Status | Phase-In Begins | Fully Phased Out |

|---|---|---|

| Single/Head of Household | $75,000 | Varies by business type |

| Married Filing Jointly | $150,000 | Varies by business type |

QBI Optimization for Colorado Springs S-Corps

Who Benefits Most:

- Sole proprietors operating as Schedule C businesses

- Single-member and multi-member LLCs taxed as partnerships

- S-corporation shareholders (on distributions, not W-2 wages)

- Real estate investors with rental properties

- Professional service providers below income thresholds

Research & Development (R&D) Expensing Restored

One of the most significant provisions for tech and innovation-focused Colorado Springs businesses is the restoration of immediate R&D expensing, which had been eliminated starting in 2022.

Key R&D Provisions:

- Small Business Retroactive Relief: Businesses with average annual gross receipts of $31 million or less can retroactively expense domestic R&D costs back to January 1, 2022

- General Expensing: All businesses can immediately expense domestic R&D costs for tax years beginning January 1, 2025 forward

- Acceleration Option: Businesses that capitalized R&D costs in 2022-2024 can elect to accelerate remaining deductions over one or two years beginning in 2025

- Foreign R&D: Continues to be amortized over 15 years

Colorado Tech & Manufacturing Businesses

What Qualifies as R&D:

- Development of new products, processes, or software

- Improvement of existing products or processes

- Prototype development and testing

- Engineering and design activities

- Quality control testing beyond routine activities

Action Item for 2022-2024 Returns: Colorado Springs businesses that capitalized R&D expenses in previous years should file amended returns or elect acceleration to capture immediate tax savings.

Business Interest Deduction (Section 163(j)) Restored

The OBBBA permanently restores the more generous EBITDA-based (Earnings Before Interest, Taxes, Depreciation, and Amortization) calculation for the business interest expense limitation under Section 163(j).

What Changed:

- Previous Rule (2022-2024): Interest deduction limited to 30% of Adjusted Taxable Income (ATI) calculated without adding back depreciation and amortization

- OBBBA Rule (2025+): Interest deduction limited to 30% of ATI calculated with depreciation and amortization added back

- Net Effect: Higher ATI = larger allowable interest deduction

Example: Real Estate Developer

A Colorado Springs real estate developer has $500,000 in interest expense and $1 million in EBITDA, but only $300,000 in taxable income after depreciation. Under old rules, they could deduct $90,000 (30% × $300,000). Under OBBBA, they can deduct $300,000 (30% × $1 million), tripling their interest deduction.

Important New Limitation: Starting in 2026, electively capitalized interest retains its character as interest and remains subject to 163(j) limitations, closing a previously available planning strategy.

SALT Cap Increase: $40,000 Through 2029

For Colorado Springs taxpayers who itemize deductions, the OBBBA temporarily increases the state and local tax (SALT) deduction cap:

| Tax Years | SALT Cap (Single/MFJ) | SALT Cap (MFS) |

|---|---|---|

| 2018-2024 | $10,000 | $5,000 |

| 2025-2029 | $40,000 (+1% annually) | $20,000 (+1% annually) |

| 2030+ | $10,000 | $5,000 |

Colorado-Specific Considerations:

- Colorado state income tax rate: 4.55%

- Colorado Springs combined sales tax rate: 8.2%

- El Paso County property taxes vary by district

- Most Colorado Springs taxpayers won't hit the $40,000 cap

Phase-Out for High Earners: The $40,000 cap reduces for taxpayers with modified adjusted gross income over $500,000 ($250,000 if married filing separately), but never drops below $10,000.

Colorado SALT Workaround Preserved

Individual Tax Provisions Affecting Business Owners

No Tax on Tips (2025-2028)

Colorado Springs restaurants, bars, salons, and hospitality businesses will benefit from the new tax treatment of tips:

Key Provisions:

- Deduction Amount: Up to $25,000 of qualified tip income is deductible

- Effective Period: January 1, 2025 through December 31, 2028

- Phase-Out: Deduction phases out at 10% for MAGI over $150,000 (single) or $300,000 (married)

- Available to All: Can be claimed regardless of standard deduction or itemizing

- Payroll Taxes Still Apply: Tips remain subject to Social Security and Medicare taxes

Impact on Colorado Springs Service Industry:

- Servers and bartenders can exclude significant tip income from federal taxation

- Employers still must withhold payroll taxes on all tips

- Tip reporting requirements remain unchanged

- Businesses should update payroll systems for 2026 withholding (no change required for 2025)

No Tax on Overtime (2025-2028)

The OBBBA introduces a deduction for qualifying overtime pay, providing relief for Colorado Springs workers and potentially affecting employer compensation strategies:

Deduction Limits:

| Filing Status | Maximum Overtime Deduction |

|---|---|

| Single/Head of Household | $12,500 |

| Married Filing Jointly | $25,000 |

| Married Filing Separately | $12,500 |

What Qualifies:

- Overtime pay must be paid at time-and-a-half or greater

- Must exceed 40 hours per week (or state standard if higher)

- Cannot be claimed on the same income as the tips deduction (no double-dipping)

- Applies to both W-2 employees and business owners paying themselves W-2 wages

Employer Payroll Considerations

Permanent Individual Tax Rate Extensions

The OBBBA permanently extends the individual tax rates and brackets established in the 2017 TCJA, which were scheduled to expire after 2025:

| Tax Rate | Single Filers (2025) | Married Filing Jointly (2025) |

|---|---|---|

| 10% | $0 - $11,925 | $0 - $23,850 |

| 12% | $11,926 - $48,475 | $23,851 - $96,950 |

| 22% | $48,476 - $103,350 | $96,951 - $206,700 |

| 24% | $103,351 - $197,300 | $206,701 - $394,600 |

| 32% | $197,301 - $250,525 | $394,601 - $501,050 |

| 35% | $250,526 - $626,350 | $501,051 - $751,600 |

| 37% | Over $626,350 | Over $751,600 |

Note: 2026 tax brackets will be adjusted for inflation and announced by the IRS in late 2025. The rates (10%, 12%, 22%, 24%, 32%, 35%, 37%) are now permanent, but the specific dollar thresholds are indexed annually.

Additional Permanent Changes:

- Standard Deduction: Enhanced amounts made permanent (2025: $15,000 single, $30,000 married; 2026 amounts will be indexed for inflation)

- Child Tax Credit: $2,000 per qualifying child made permanent

- Alternative Minimum Tax: Higher exemption amounts preserved

Estate and Gift Tax Exemption Increase

Effective January 1, 2026, the OBBBA significantly increases estate and gift tax exemptions:

| Tax Year | Individual Exemption | Married Couple |

|---|---|---|

| 2025 | $13.99 million | $27.98 million |

| 2026+ | $15 million | $30 million |

Planning Implications for Colorado Springs Business Owners:

- Family business succession planning becomes more flexible

- Larger estates can transfer tax-free to heirs

- Annual gift exclusions remain at $18,000 per recipient (2024), indexed for inflation

- Generation-skipping transfer tax exemption also increases to $15 million

Business Succession Planning

Qualified Small Business Stock (QSBS) Enhanced Benefits

For Colorado Springs startups and small C-corporations, the OBBBA significantly enhances Section 1202 QSBS benefits:

What Changed:

| Provision | Pre-OBBBA | Post-OBBBA (After 7/4/25) |

|---|---|---|

| Exclusion Limit | $10 million or 10× basis | $15 million or 10× basis |

| Gross Assets Test | $50 million | $75 million |

| Gain Exclusion | 100% | 100% |

| Holding Period | 5 years (100% exclusion) | Tiered: 3/4/5 years (see below) |

NEW: Tiered Holding Period System (Stock Acquired After July 4, 2025):

The OBBBA introduces a revolutionary change to QSBS holding requirements, allowing earlier capital gains exclusions:

| Holding Period | Exclusion Percentage | Example: $15M Gain |

|---|---|---|

| 3 Years | 50% | $7.5M excluded, $7.5M taxable |

| 4 Years | 75% | $11.25M excluded, $3.75M taxable |

| 5+ Years | 100% | $15M excluded, $0 taxable |

Critical QSBS Timing Rule

Strategic Planning Opportunities:

- Earlier Liquidity Events: Founders can now realize substantial tax-free gains after just 3 years instead of waiting 5 years

- Staged Sales: Sell 50% at 3 years, hold remaining shares for full exclusion at 5 years

- Partial Exits: Investors can exit earlier with meaningful tax benefits while maintaining upside

- M&A Timing: Acquisition discussions can start earlier knowing partial exclusion is available

Requirements for QSBS Treatment:

- Must be C-corporation stock (not S-corp or LLC)

- Stock must be acquired directly from the corporation (not secondary purchase)

- At least 80% of assets used in active business operations

- Cannot be certain excluded industries (financial, hospitality, professional services)

- Gross assets cannot exceed $75 million after stock issuance

Planning Opportunity: Colorado Springs tech startups, manufacturing companies, and product-based businesses should evaluate C-corporation structure to potentially exclude up to $15 million in capital gains when selling the business. With the new tiered holding period system, founders can now access meaningful tax benefits (50% exclusion) after just 3 years, making QSBS significantly more attractive for growth companies planning near-term exits.

Temporary Provisions: Plan Before They Expire

Provisions Expiring December 31, 2028

Several valuable provisions sunset after 2028, creating a planning window for Colorado Springs businesses:

2025-2028 Temporary Provisions

Planning Strategy: Colorado Springs businesses should maximize use of temporary provisions through 2028 while preparing for their expiration. Consider accelerating major equipment purchases or business expansion plans to capture full benefits.

Provisions Expiring December 31, 2029

- $40,000 SALT Cap: Reverts to $10,000 starting 2030

- Enhanced SALT Benefits: High-earning itemizers should consider multi-year tax planning

Colorado-Specific Implementation Considerations

State Conformity Issues

Colorado's tax code automatically conforms to most federal tax changes, but some provisions require specific state action:

Automatic Conformity:

- Bonus depreciation follows federal treatment

- Section 179 expensing generally conforms (with Colorado-specific limitations)

- QBI deduction flows through to Colorado return

- Federal AGI changes affect Colorado taxable income

Potential Non-Conformity:

- Colorado may not conform to tips and overtime deductions (pending state legislation)

- State PTET election remains available regardless of federal SALT cap changes

- Colorado has separate rules for enterprise zone credits and other state-specific incentives

Colorado Legislative Updates

El Paso County Business Considerations

Colorado Springs and El Paso County businesses should consider these local factors when implementing OBBBA tax strategies:

- Military Community: Large military presence may affect workforce planning around overtime provisions

- Hospitality & Tourism: Tips deduction particularly valuable for restaurants, bars, hotels, and tourist attractions

- Tech & Aerospace: R&D expensing restoration benefits growing technology sector

- Real Estate Development: Bonus depreciation and interest deduction changes impact commercial projects

- Professional Services: QBI deduction planning critical for CPAs, attorneys, consultants above income thresholds

Action Plan: What Colorado Springs Businesses Should Do Now

Immediate Actions (Before December 31, 2025)

- Equipment Purchase Analysis

- Evaluate accelerating planned 2026 equipment purchases into 2025

- Model Section 179 vs. bonus depreciation for optimal tax benefit

- Consider vehicle purchases under enhanced depreciation rules

- Ensure property is placed in service before year-end to qualify

- R&D Cost Review

- Identify all qualifying research expenses from 2022-2024

- Determine if small business exception applies (under $31M average gross receipts)

- File amended returns for 2022-2024 if beneficial

- Elect acceleration of capitalized R&D costs from prior years

- Implement proper tracking systems for ongoing R&D activities

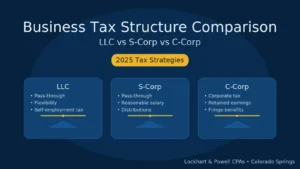

- Entity Structure Evaluation

- Review whether S-corp vs. C-corp structure maximizes OBBBA benefits

- Consider QSBS election for qualifying C-corporations

- Evaluate reasonable compensation strategies for QBI optimization

- Assess whether Colorado PTET election makes sense

- Payroll System Updates

- Review employee tip reporting procedures

- Verify overtime tracking systems are accurate

- Communicate new deduction opportunities to employees

- Update payroll software for 2026 withholding changes

2026 Planning Priorities

- Multi-Year Tax Projections

- Model tax liability for 2026-2030 under various scenarios

- Plan for 2028/2029 expirations of temporary provisions

- Evaluate timing of major business decisions (equipment, expansion, succession)

- Consider Roth conversion opportunities with permanent lower rates

- Estate Planning Review

- Update estate plans to reflect $15 million exemption

- Consider gifting strategies for family business succession

- Review life insurance needs with higher exemptions

- Implement valuation discounts where appropriate

- Business Financing Strategy

- Leverage improved interest deduction limits for expansion financing

- Evaluate debt vs. equity financing with Section 163(j) changes

- Consider real estate acquisitions with enhanced depreciation benefits

- Model cash flow impact of accelerated deductions

Year-End Tax Planning Deadline

Industry-Specific Strategies for Colorado Springs Businesses

Restaurants & Hospitality

Hospitality Industry Action Items

Construction & Trades

- Equipment Strategy: Maximize Section 179 and bonus depreciation for trucks, machinery, tools

- Overtime Planning: Many construction workers will benefit from overtime deduction

- Entity Structure: Evaluate S-corp election if operating as sole proprietor or partnership

- Real Estate: Consider separate entity for equipment rental to property management company

Professional Services (CPAs, Attorneys, Consultants)

- QBI Optimization: Critical to manage income around phase-out thresholds

- Reasonable Compensation: Balance W-2 salary vs. distributions for S-corps

- Equipment Purchases: Office furniture, computers, software qualify for expensing

- SALT Cap: Higher earners benefit from $40,000 cap through 2029

Technology & Manufacturing

- R&D Expensing: Immediately deduct software development and product research costs

- QSBS Election: Consider C-corp structure for potential $15M gain exclusion with tiered benefits (50% at 3 years, 75% at 4 years, 100% at 5 years)

- Manufacturing Structures: Full expensing available for construction begun before 2029

- Equipment Leasing: Evaluate purchase vs. lease with enhanced depreciation

Real Estate Investors & Developers

- Bonus Depreciation: Full expensing on equipment, appliances, fixtures

- Interest Deduction: EBITDA-based calculation significantly increases allowable deduction

- QBI Deduction: Rental real estate may qualify as trade or business

- Section 1031 Exchanges: Consider timing with depreciation strategies

Common Mistakes to Avoid

OBBBA Implementation Pitfalls

How Lockhart & Powell Can Help

The One Big Beautiful Bill Act represents the most complex tax legislation in nearly a decade, with provisions affecting every Colorado Springs business from sole proprietors to established corporations. As experienced CPAs serving El Paso County for nearly 40 years, Lockhart & Powell has the expertise to help you navigate these changes and maximize your tax savings.

Our OBBBA Services Include:

- Comprehensive Tax Impact Analysis: Detailed modeling of how OBBBA provisions affect your specific business situation

- Equipment Purchase Planning: Strategic timing and structuring of capital expenditures to maximize Section 179 and bonus depreciation benefits

- R&D Cost Recovery: Identification of qualifying research expenses and preparation of amended returns for 2022-2024

- Entity Structure Optimization: Evaluation of S-corp, C-corp, partnership, and sole proprietorship structures under new law

- QBI Deduction Maximization: Strategies to optimize the 20% pass-through deduction while managing income thresholds

- Multi-Year Tax Projections: Planning that accounts for temporary provisions expiring in 2028 and 2029

- Colorado Conformity Guidance: Expert navigation of state-specific tax implications

Free OBBBA Impact Assessment

Frequently Asked Questions

Q: When does the One Big Beautiful Bill Act take effect?

A: The OBBBA was signed into law on July 4, 2025, but different provisions have different effective dates. Many business provisions (like 100% bonus depreciation) apply retroactively to property acquired on or after January 20, 2025. Individual provisions like tips and overtime deductions begin January 1, 2025. Some provisions don't start until 2026 or later.

Q: Can I claim both Section 179 and bonus depreciation on the same equipment?

A: Yes, you can use both on the same property. Typically, you'd apply Section 179 first up to its $2.5 million limit, then use bonus depreciation for any remaining basis. However, you should work with a CPA to determine the optimal strategy based on your income, business structure, and future tax planning.

Q: Does Colorado conform to all OBBBA provisions?

A: Colorado generally conforms to federal tax law changes, but conformity isn't always automatic. The state typically addresses conformity during the spring legislative session. Bonus depreciation, Section 179, and QBI deduction generally flow through to Colorado returns, but tips and overtime deductions may require specific state legislation.

Q: How does the R&D expensing restoration work for small businesses?

A: If your business has average annual gross receipts of $31 million or less, you can retroactively deduct domestic R&D costs for tax years beginning January 1, 2022 and later. This means you can file amended returns for 2022, 2023, and 2024 to claim immediate deductions instead of the required amortization. Larger businesses can immediately expense R&D starting in 2025.

Q: What happens when temporary provisions expire in 2028?

A: The tips deduction, overtime deduction, auto loan interest deduction, and several other provisions expire December 31, 2028. Unless Congress extends them, these benefits will no longer be available starting in 2029. Businesses should plan accordingly and not assume these provisions will continue beyond 2028.

Q: Can S-corporation owners benefit from the QBI deduction?

A: Yes, S-corporation shareholders can claim the 20% QBI deduction on their share of business income, but only on distributions, not on W-2 wages paid to themselves. This creates a balancing act: higher salary reduces QBI but may save self-employment taxes; lower salary increases QBI but the IRS requires "reasonable compensation." Colorado Springs S-corp owners should work with a CPA to optimize this balance.

Q: How do I know if my business qualifies for the small business R&D exception?

A: You qualify if your average annual gross receipts for the three prior tax years are $31 million or less. For example, a business filing a 2025 return would average gross receipts from 2022, 2023, and 2024. If that average is under $31 million, you can elect to immediately expense R&D costs retroactive to 2022.

Q: Will the OBBBA affect my 2025 tax return?

A: Yes, significantly. Many provisions apply retroactively to January 1, 2025 or January 20, 2025. When you file your 2025 tax return in early 2026, you can claim 100% bonus depreciation, enhanced Section 179, tips deduction, overtime deduction, and other benefits. This makes year-end 2025 planning critical.

Conclusion: Taking Action on the One Big Beautiful Bill Act

The One Big Beautiful Bill Act represents a once-in-a-generation opportunity for Colorado Springs small businesses to significantly reduce their tax burden through strategic planning and timely action. From immediate equipment expensing to permanent QBI deduction benefits to temporary provisions like tips and overtime deductions, the OBBBA touches virtually every aspect of business taxation.

However, the complexity of these provisions—combined with retroactive effective dates, sunset provisions, and the interplay between different deductions—makes professional guidance essential. A misstep in applying Section 179 vs. bonus depreciation, missing retroactive R&D opportunities, or failing to optimize entity structure could cost your business tens of thousands of dollars in lost tax savings.

As Colorado Springs' trusted CPA firm for nearly 40 years, Lockhart & Powell has the expertise and local knowledge to help your business navigate the OBBBA and maximize your tax benefits. We've already helped dozens of El Paso County businesses implement OBBBA strategies, and we're ready to create a customized plan for your business.

Don't Wait—Act Now

Lockhart & Powell CPAs has served Colorado Springs businesses for nearly 40 years, providing strategic tax planning, compliance, and advisory services. Our team stays current on all federal and Colorado tax law changes to ensure our clients maximize every available deduction and credit. Contact us at (719) 578-8200 or visit our Colorado Springs office to discuss how the One Big Beautiful Bill Act can benefit your business.